Key Takeaways

- Early settlement of a car loan in Singapore does not automatically result in meaningful interest savings.

- Loan structures such as the Rule of 78, commonly used in some car loans, can significantly limit savings from early repayment.

- Loan penalty charges and administrative fees often reduce the financial benefit of settling early.

- Paying off a car loan early may create cash flow strain if liquidity is not carefully considered.

- The right decision depends on timing, loan terms, and personal financial priorities rather than myths.

Should You Repay Your Car Loan Early in Singapore?

In Singapore, early settlement of a car loan is often viewed as a financially savvy move. In reality, several misconceptions can lead to disappointment or even unexpected costs.

Many car owners in Singapore assume that paying off their loan early will automatically save them on interest. Unfortunately, penalties, interest structures, or opportunity costs might rake up a larger bill in the long run.

This article unpacks the most common myths surrounding early loan settlement, explains how car loans are structured in Singapore, and clarifies when early repayment may or may not make sense.

Myth 1: Early Settlement Always Saves You Money

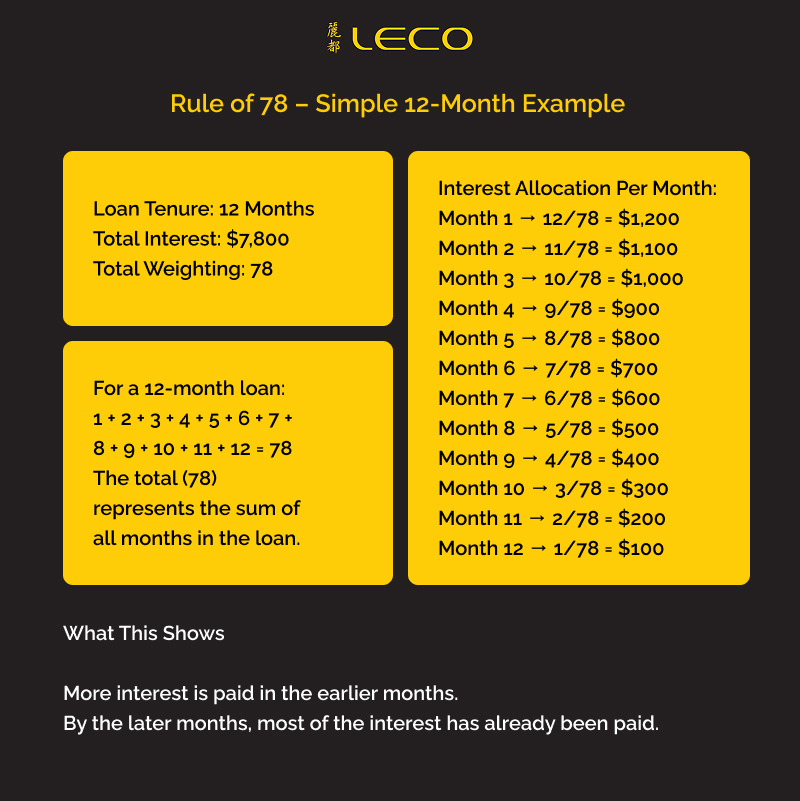

One of the most persistent myths is that settling a car loan early in Singapore will significantly reduce total interest paid. In reality, many car loans are structured with interest calculated upfront. What this means is that paying off your loan early may not reduce your total interest, since a significant portion of the interest has already been accounted for at the start of the loan.

A common example is the rule of 78 method for car loans, where a higher proportion of interest is effectively allocated to the earlier part of the loan tenure. When this structure is used, settling the loan early often results in smaller interest rebates than borrowers expect.

For drivers who are already midway or late into their loan tenure, the remaining interest savings may be minimal after adjustments. This can be particularly frustrating for those who anticipate a substantial reduction in their settlement amount.

Myth 2: Paying Off Early Is Always the Financially Smart Choice

Another widespread assumption is that eliminating debt as quickly as possible is always the best financial decision. While being debt-free feels reassuring, early repayment may not be optimal in every situation.

Paying off a car loan early ties up cash that could otherwise be used for emergency funds, business needs, or investment opportunities.

This is especially relevant for owners of higher-value vehicles, such as a Toyota Vellfire, where the upfront loan amount is substantial, and cash flow flexibility matters more than interest savings alone.

Understanding Loan Penalties and Settlement Fees

Uncertainty around loan penalty charges is a major reason early settlement causes dissatisfaction. Many borrowers underestimate how charges affect the final settlement figure.

Penalties may include administrative fees, early termination charges, or reduced interest rebates, depending on the lender’s terms. These charges vary across banks and finance companies, making it essential to request a formal settlement quotation.

Without clear figures, borrowers may believe they are saving money when the net benefit is marginal or even negative after penalties are applied.

Loan terms can also differ depending on where the vehicle was purchased. Cars bought through a parallel importer may be financed via different financial institutions or structured packages compared to authorised dealerships. While the core principles remain similar, borrowers should review their specific loan agreement carefully, as settlement terms and rebate calculations may vary.

Interest Savings From Early Repayment Are Not Guaranteed

The concept of interest savings from early repayment is appealing, but it depends heavily on how the loan is structured and how early the settlement occurs.

Borrowers who settle very early in the loan tenure may see some savings, but even then, the difference may be smaller than expected. Those closer to the end of their loan period often find that most of the interest has already been accounted for.

Understanding how interest is calculated is more important than focusing solely on the idea of early repayment itself.

When Early Settlement May Make Sense

Early settlement can still be appropriate in certain scenarios. It may suit borrowers who are nearing the end of their loan tenure, have excess cash reserves, or are planning to sell or replace their vehicle.

Drivers who prioritise reducing monthly commitments or simplifying finances may also find value in settling early, even if the interest savings are limited. This can be relevant when restructuring ownership, especially when purchasing through a reliable parallel importer in Singapore, where loan arrangements may differ slightly from authorised dealers.

When Early Settlement May Not Be Ideal

Early settlement may not be suitable for drivers who are still early in their loan term, face high penalties, or rely on cash for other financial goals. It may also be less appealing for those who value liquidity and flexibility over psychological comfort.

For some borrowers, maintaining manageable monthly repayments while preserving cash reserves offers greater financial resilience than eliminating the loan.

Making the Right Decision With Clear Information

The real question is whether early settlement aligns with your personal financial situation. Myths often oversimplify a decision that depends on loan structure, timing, cash flow, and risk tolerance.

If you are considering early settlement of a car loan in Singapore, seek clarity before committing. Review your loan agreement carefully, request a settlement quote, and assess how the decision fits within your broader financial plans.

At Leco Auto, we understand the true costs and trade-offs of paying off your loan. Speak to us for guidance to ensure you make an informed decision that is intentional and aligned with your long-term priorities.